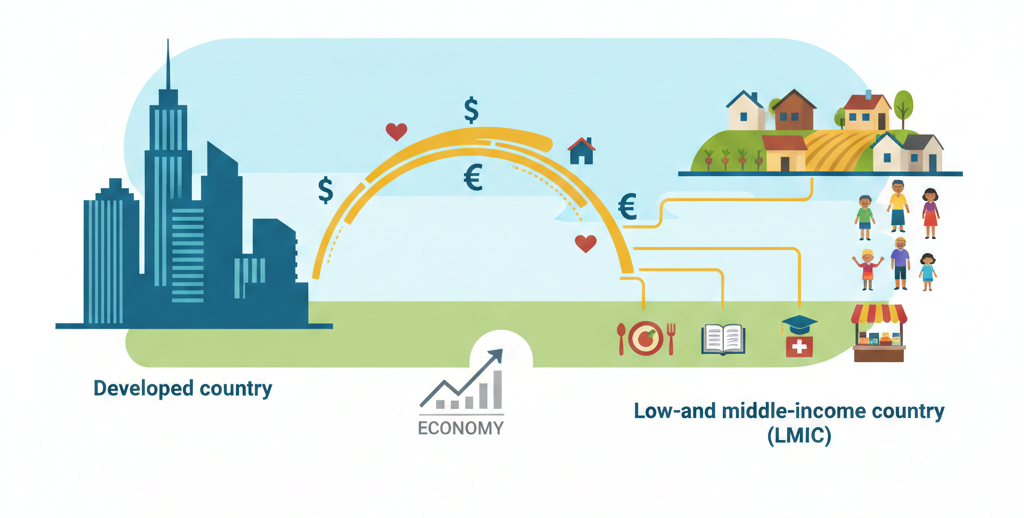

In 2022, remittances to low- and middle-income countries (LMICs) surpassed foreign direct investments. And ever since, it has continued to outpace both official development assistance (ODA) and FDI to LMICs combined, according to the World Bank.

By 2024, approximately $905 billion was sent around the world in remittances, with about $685 billion (75.7%) going to LMICs.

For context, the EU mapped €1.9 billion for its 2026 humanitarian aid budget for Africa, the Middle East, Ukraine, Southeast Asia and the Pacific, Moldova, Central America, South America, and the Caribbean.

Clearly, remittances, the money people living abroad send back home, are undeniably a substantial structural feature of the global economy.

It is also an indicator of migration patterns.

Countries with high emigrant populations, especially developing countries (such as India, Mexico, and the Philippines), typically top the chart of remittance-receiving countries. Similarly, countries with high immigrant populations (such as the US, Saudi Arabia, and Switzerland) are topping the remittance-sending charts.

Basically, as more people migrate from developing to developed countries to work, more remittances tend to flow from the developed countries to developing countries, helping support families and communities in migrants’ home countries.

What does this mean for the receiving families, communities, and countries?

Remittances as Immediate Economic Stabilizers

About 800 million people (~9.6% of the global population) benefit directly from remittances sent by their family members working abroad.

A large portion of remittances received goes into financing basic needs like food, shelter, healthcare, and education.

Remittances also act as a lifeline for families struggling to make ends meet, ensuring that they:

- Sustainably live through phases of unemployment

- Do not sell off their assets during shocks

- Have extra cash to spare for other goods and services that can improve their quality of life.

With extra cash at hand, recipient families usually have higher purchasing power than their counterparts.

In turn, higher purchasing power leads to a multiplier effect.

Since recipients have more to spare, they tend to spend more within their communities. The more money they spend on small local businesses, the more the businesses can:

- Pay their workers better or even employ more workers

- Purchase more goods and expand their business

- Patronize more suppliers who source products from both local and international manufacturers.

In essence, remittances help improve purchasing power, which in turn helps maintain demand in local markets and ensure the survival of local businesses.

From a broader perspective, this cycle further bolsters domestic economies, helping them avoid contraction during crises.

Financing Microenterprise and Risk-Taking

Remittances are not all about consumption.

While about 75% of remittances inflows to LMICs directly support household consumption, the remaining 25% goes to savings and investments.

Typically, these investments often focus on funding, founding, or expanding necessity-based small businesses that meet the popular demands of local communities.

In agricultural communities, for instance, this could mean buying, selling, or servicing agricultural equipment, opening stalls for buying and selling farm produce, or funding seasonal farming.

Fundamentally, higher remittance inflows can translate into greater capital access, which can boost recipients’ confidence in undertaking new ventures. Thus, leading to more small businesses springing up locally.

Strengthening National Financial Systems

The impacts of remittance inflows can extend beyond local economies to state, national, and even regional economies.

In countries like Guatemala, for instance, where remittances make up nearly 20% of GDP, there has also been a significant increase in foreign reserves holdings, according to the IMF.

As remittances become a significant factor at a broader scale, nations often have to adjust policies or strategies to maximize opportunities and outcomes as a result of:

- Remittance inflows stabilizing exchange rates: As more and more foreign currencies are converted into the local currency, the local currency tends to appreciate or stabilize against foreign currencies.

- Remittances supporting balance of payments: Remittance inflows establish a balance between financial inflows and outflows in a given country. Additionally, increased remittance inflows also translate to significant improvement in recipient countries’ national current account balance as well as deposits in financial institutions.

- Remittances reducing reliance on external borrowing: Unlike most other external financing sources, such as loans and foreign aid, remittances do not come with interest and extra debt burdens.

With all these in mind, it is usually in the best interest of financial institutions and operators in receiving countries to create environments that support more remittance inflows and boost national foreign income.

Mexico, for example, stands out as one of the most competitive remittance markets worldwide, due to various policies and strategies (such as remote account opening and Directo a México) employed by its financial institutions to ease remittance costs and make transfers more seamless.

These measures also strengthen local financial institutions to compete in the global market.

However, despite efforts in this direction, remittance costs still remain relatively higher than the 3% (of total costs) targeted in the UN SDG.

In Mexico, service costs take up nearly 5% of the total transaction amount. In Guatemala, the average cost hovers around 4.19% of the total transaction amount.

To keep costs down and improve client satisfaction, local financial institutions sometimes establish direct partnerships with international remittance service providers, cutting out third-party services that can increase costs.

A good example is the BOSS Money-Banrural partnership in the US-Guatemala remittance corridor, which allows Guatemalans in the US to send money to Banrural for as low as $0 (0% of the total transaction amount) for first transactions.

When local financial systems are strengthened to provide better, more affordable services to customers at home and abroad, every cent saved adds to long-term economic gain at a national scale.

Human Capital as Long-Term Economic Gain

As more money is saved when sending remittances, the ripple effects result in increased spending for better education, better healthcare, and better investments that boost human capital development.

For the beneficiaries, access to better quality services can significantly increase their potential to earn higher than they most likely would have if remittances didn’t fund the access.

For nations, this means access to a better-educated and more productive workforce that can substantially drive and sustain economic growth and stability over time.

The Real Limitation and Why It Still Matters

For as much as remittances have a sweeping positive impact on the economy, they come with some concerns.

In countries like Tajikistan and Lebanon, where remittances account for over 30% of GDP, economic stability could easily be threatened by a slight change in remittance behaviors due to external factors, such as remittance policies imposed by sending countries.

Moreover, dependency on remittance as a major source of external finance could mask the effects of foundational governance problems, creating an economic bubble that is only sustained for as long as remittance flows remain consistent.

Lastly, studies have found that remittances sometimes have negative effects on local labor markets, particularly in cases where recipients perceive remittances as a substitute for wages or where remittances far outweigh local wages.

In fact, the higher the remittance per capita, the lower the employment rate.

The volatility of remittances is a cause for direct recipients and economies to not depend on but rather see remittances as a complementary source of finance.

Conclusion

Remittances have a widely positive impact that can go a long way to improve the lives of recipients and boost local, national, and regional economies.

At the microeconomic level, it fosters financial inclusion and increases access to quality food, shelter, healthcare, education, and other necessities. It also boosts purchasing power, fueling rural and local economies.

At the macroeconomic level, impacts manifest in strengthened financial systems reflected in stable exchange rates, balance of payments, bank deposits, and reduced reliance on external borrowing.

The impacts at different economic levels merge to institute long-term economic gains across the board.

However, despite all the benefits, there is still cause for beneficiaries not to depend on remittances as a primary source of finance, as fluctuations in remittances could result in immediate, wide-scale negative impacts across the board.

Established in December 2008, The Diplomatic Insight is Pakistan’s premier diplomacy and foreign affairs magazine, available in both digital and print formats.